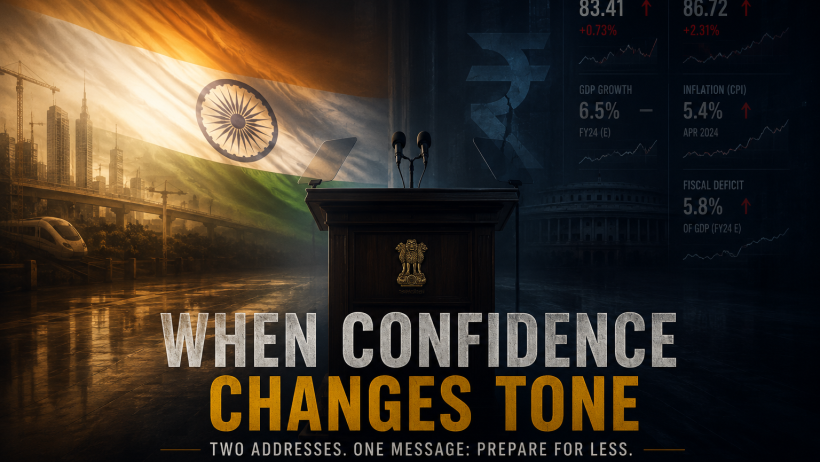

Two Addresses. One Message: Prepare for Less.

Signal-Talk Analysis · Twice in quick succession, Indian Prime Minister addressed the nation invoking restraint, discipline, austerity, and collective sacrifice. On the surface, the message appears responsible — even prudent. But in cybernetic systems, repetition is rarely accidental, and systems reveal themselves not just through numbers — but also through tone. Because systems often attempt to manage expectations emotionally before economic stress becomes fully visible numerically.

And, when governments begin emotionally preparing citizens before visible pain arrives, it often signals deeper stress beneath the dashboard. That’s the signal being read in this episode; 13 May 2026; ST -033/ NV Subba Rao (read time: 11 mins).

NV Subba Rao is the author of Quo Vadis? Uncle Sam 2.0 — a social media and systems-level exploration of power, media, and democracy in the algorithmic age.

Available on Amazon

Website: UncleSam2.com

WHEN CONFIDENCE CHANGES TONE… what has shifted.?

For nearly a decade, the dominant Indian narrative was expansion.

Fastest-growing major economy.

Digital rise.

Infrastructure boom.

Global leadership summits.

Space missions.

Manufacturing ambitions.

A confident India stepping onto the world stage, and much more…

The messaging was aspirational, assertive, and upward. India was not merely growing it was projecting inevitable certainty— Its time had come; the world needs India, and there were slogans and memes for every occasion.

The loud and repeated assertions by the PM landed as poetry + music to large swathes of its citizens, both at home and abroad.

And suddenly, the tone has changed – with repeated calls for austerity. When governments begin emotionally preparing citizens before visible pain fully arrives, it often signals deeper stress beneath the dashboard.

What then do these repeated calls for restraint reveal about the economy? Is this fiscal discipline, psychological conditioning, or early crisis management?

Importantly, this episode intentionally steps away from the larger ideological noise:

- religious polarization,

- Akhand Bharat rhetoric,

- perpetual election-mode nationalism,

- personality cult dynamics,

- media spectacle,

- inconsequential ministries.

- sloganeering, outrage ecosystems, and related.

Not because those forces are irrelevant. But because they can overwhelm weaker economic signals that are seemingly emerging from the underlying system layer.

The economic backdrop is what matters more:

- A rupee that has depreciated nearly 35–40% against the dollar over the last decade, with growing public anxiety around the psychological ₹100/$ threshold

- Questions emerging around India’s path to becoming a fully developed economy by 2031–2040. They are beginning to stretch outward – amid slowing global demand and domestic inequality pressures.

- The $5 trillion economy now appears as a distant dream even post 2031 – given the Rupee’s periodic pressure against the dollar

- Oil and energy volatility tied to geopolitical instability triggering Supply-chain uncertainty across global corridors.

- With crude oil prices periodically spiking 15–25% during geopolitical disruptions, the direct stress on India’s import bill and currency stability gets accentuated further with hikes in fuel prices

- Merchandise export growth slowing unevenly across sectors even as global trade fragmentation intensifies

- MSMEs — contributing nearly 30% of India’s GDP and ~45% of exports — continuing to face pressure from:

- weak domestic consumption,

- high borrowing costs,

- digital compliance burdens,

- and cheaper import competition

- MSMEs — contributing nearly 30% of India’s GDP and ~45% of exports — continuing to face pressure from:

- Persistent unemployment and underemployment, particularly among youth, despite headline GDP growth remaining in the 6–7% range

- Uneven GDP growth increasingly concentrated in premium and asset-owning segments, with wealth concentration accelerating sharply:

- Consumption growth consequently appears strongest in:

- premium housing,

- luxury retail,

- financial assets,

- high-end travel,

- and upper-tier urban consumption,

- while mass-market demand remains uneven and periodically weak across:

- FMCG,

- entry-level automobiles,

- small retail,

- rural consumption,

- and informal sectors

- Domestic inequality widening between capital owners and wage earners.

- India’s per-capita income still remains around $2,700–3,000 annually, placing the country roughly in the lower-middle tier globally (around ~130th–140th range depending on methodology and PPP adjustments) — well below developed-economy thresholds despite India being among the world’s largest aggregate GDP systems.

- Income and wealth inequality indicators, including the Gini coefficient (~0.41–0.43 depending on methodology), continue to suggest widening asymmetry between asset owners and wage earners — even as headline GDP growth remains relatively strong.

- While India’s consumption-based Gini coefficients have moved only modestly, wealth concentration at the top has intensified more sharply during the same period, even as headline GDP growth remained relatively strong.

- Consumption growth consequently appears strongest in:

- Fiscal balancing pressures intensifying as the state attempts to simultaneously fund:

- mega infrastructure ambitions (public CapEx growth ~15%+ YoY),

- mass welfare obligations (₹4–5 lakh crore subsidy layers continuing),

- rising defense preparedness (~8–10% annual spending increases),

- and politically competitive populism (free power, cash transfers, loan waivers, 800 million on free food schemes, and expanding state-level giveaways)

- all while attempting to contain fiscal deficits near the ~5% of GDP range (FY 26 budget 4.4%), limiting the government’s room to absorb future economic or geopolitical shocks, along with elections and welfare commitments — and doing so without resorting to printing more money or increasing borrowing pressure.

- Foreign exchange reserves remain large on paper — nearly $697 billion with ~8 months of import cover — but are increasingly functioning as defensive buffers against:

- imported oil shocks (~85% crude import dependence),

- rapid hot-money exits (~₹2 lakh crore FPI outflows in recent months),

- and rupee volatility (every ~5% depreciation sharply inflating India’s import bill and inflation sensitivity).

- Regional diplomacy appearing more fragile despite ambitions of larger geopolitical influence, with neighborhood relations often oscillating between strategic caution and rhetorical assertion — even as South Asia remains one of the least economically integrated regions in the world. The Intra-South Asian trade still accounts for only about 5–7% of the region’s total trade, compared with roughly:

- 25% in ASEAN, and 50–60%+ within the EU.

- India’s trade with its immediate neighborhood has generally remained only around ~2–4% of its total global trade over much of the last decade, despite geographic proximity and significant market potential. Multiple studies estimate South Asia’s unrealized regional trade potential at roughly 2–3x current levels, constrained by:

- political tensions,

- border frictions,

- tariff and non-tariff barriers,

- weak logistics integration,

- and trust deficits.

- The resulting opportunity cost is not merely diplomatic. It affects:

- export resilience,

- supply-chain depth,

- currency buffers,

- energy cooperation,

- and regional economic shock absorption.

- Rising global fragmentation and war-risk premiums

- Public discourse increasingly dominated by:

- identity politics,

- religious polarization,

- cult-like political amplification,

- and algorithm-driven outrage cycles

On balance, the resulting signal is subtle but important: a high-growth economy can still experience widening psychological and economic divergence between:

- the “India that invests,” and the

- “India that consumes to survive.”

Apropos, India may still be growing. But the system appears to be also recalibrating expectations – as austerity has suddenly entered prime-time politics.

And that changes the signal.

SIGNAL

What actually matters?

NOISE

What distracts and distorts?

1. The Govt. may be preparing citizens psychologically

Economic slowdowns are easier to manage when public expectations soften before hardship intensifies. Austerity messaging often functions as narrative cushioning.

2. Fiscal Stress Signals May Be Emerging

Repeated calls for restraint can indicate concern around:

- welfare-versus-growth tradeoffs

- subsidy burdens

- oil import exposure

- currency stability

- debt servicing pressures

3. The Leadership Narrative Has Shifted

The earlier rhetoric centered around aspiration:

“Build more. Consume more. Rise faster.”

The current undertone feels different:

“Conserve. Endure. Adjust.”

That tonal migration itself is the signal.

4. Global Instability Is Entering Domestic Messaging

Wars, shipping disruptions, commodity volatility, and deglobalization are no longer external stories.

They are entering kitchen economics.

Fuel. Food. Fertilizer. Freight.

5. Systems Under Stress Often Turn Moral

When hard economics becomes difficult to communicate, systems frequently frame restraint as virtue:

- sacrifice

- nationalism

- discipline

- duty

- collective resilience

This helps stabilize social sentiment.

At least temporarily.

1. Symbolism Without Structural Reform

Citizens being asked to consume less while systemic inefficiencies remain untouched creates distrust.

2. Elite Immunity

Austerity narratives lose legitimacy when luxury consumption and political spectacle continue uninterrupted at the top.

3. GDP Headlines May Mask Ground Reality

Aggregate growth can coexist with:

- weak household savings

- stagnant wages

- job insecurity

- shrinking discretionary spending

The premium economy is not the popular economy.

4. Media Amplification Without Transparency

If messaging emphasizes emotional sacrifice but avoids granular economic clarity, public anxiety eventually rises.

5. Temporary Narrative Management

Sometimes repeated messaging is less about long-term reform and more about short-term perception stabilization.

That distinction matters

6. Supporters Interpret the Message Differently

Some supporters of the Prime Minister (as evinced on prime-time media) argue that the messaging is aimed less at the economically vulnerable and more at affluent and consumption-heavy segments of society. Particularly around visible excess, wasteful consumption, energy usage, and imported luxury dependence.

The more emotionally invested sections of the support base may also view such messaging through a broader lens of national discipline, sacrifice, and leadership trust, placing greater emphasis on intent and symbolism than on near-term economic discomfort.

SYSTEM LENS The deeper structural view

Strong systems do not merely ask citizens to prepare for less

– In cybernetic systems, tone shifts are feedback signals.

Further leaders who project confidence rarely pivot repeatedly toward restraint unless:

- external stress is rising,

- internal buffers are weakening,

- or future turbulence is anticipated.

Leaders rather typically expand productive capacity fast enough, so that restraint remains temporary rather than structural.

Because confidence eventually is not maintained through slogans and speeches alone.

It is maintained when citizens feel:

- opportunities widening,

- incomes strengthening,

- volatility reducing,

- and the future expanding rather than narrowing.

The important question is not whether austerity is “good” or “bad.”

The real question is:

What is the system seeing that citizens are only beginning to feel?

The language often changes first, and the economics follows soon enough.

SIGNAL-to-NOISE RATIO (SNR)

Editorial Score: 7.4/ 10

Low 1-3

Medium 4-6

High 7-9

Perfect 10 (no Noise)

Scale:

1 = Number detached from context (multiple meanings, speculation high): noise-dominant system

10 = Number grounded in context: No Speculation – signal-dominant system

Interpretation: At SNR 7.4, this is a strong signal and suggests a significant intent. The repetition, timing, and tonal shift indicate this is more than symbolic rhetoric. The signal appears to indicate:

- expectation recalibration,

- fiscal caution,

- and preparation for a more constrained global-economic environment.

However, the absence of full transparency and structural clarity still leaves substantial noise in the system.

Comparative Signal-to-Noise (SNR) Scores

How different actors frame the same issue—measured using the same Signal-to-Noise logic.

Editorial (Signal-Talk)

7.4

Strong Signal: Alert and a warning of eco distress in system

Experts Score (WhatsApp Economy groups (base 22))

8.2

Gen AI-5 (LLM ‘s synthesis – Avg. score) #

7.1

Chat Gpt 7.1, Grok 7.5, Perplexity 7.0, Gemini 6.8, Claude 6.9.

Reader’s Pulse (Poll)

(Scale: 1 = Sys deplelting, 10 = Sys forming)

* Poll scores are dynamic- and changes with responses (Please see + take the poll below)

# Gen AI-5 is average score of 5 LLM’s – Chat GPT, Grok, Gemini, Perplexity, and Claude

SNR scores are on scale of 1-10 (1 = System depleting and 10 System forming. in this case 1 = High confidence in economy: ideological noise – interpretation not aligned to PMs messaging; 10= Low confidence in economy signal – Early distress warnings interpretation aligned to PM’s messaging.

How clearly do you feel about the repeated austerity messages from the PM – after reading this episode of Signal-Talk?

Cast your vote and see how your score compares with Community and Gen AI scores.

CAST YOUR VOTE

Rate the signal, not the sentiment (Your rating and email are kept confidential and not shared with anyone)

Your take: INDIAN ECONOMY – WHEN CONFIDENCE CHANGES TONE: What’s in the new signal?

(Scale: 1 = Sys deplelting, 10 = Sys forming)

System Response

If the signal is genuine – signaling the need for austerity measures, the response cannot remain symbolic.

The system would need to ensure:

1. Employment Generation Must Outpace Demographic Pressure: India adds roughly 10–12 million working-age citizens annually.

The challenge is no longer merely creating jobs —

but creating:

- productive,

- wage-growing,

- consumption-sustaining jobs.

Particularly across:

- manufacturing,

- MSMEs,

- logistics,

- construction,

- exports,

- and technology-enabled services.

Without stronger employment velocity, GDP growth risks becoming increasingly asset-led rather than livelihood-led.

2. Broad-Based Consumption Must Rebalance

Premium consumption alone cannot sustainably carry a $4 trillion+ economy.

The system may need to revive:

- rural demand,

- entry-level consumption,

- affordable housing,

- small retail,

- and mass-market purchasing power.

Especially when:

- the top 1% control ~40%+ of wealth,

- the top 10% control roughly 70–77% of wealth while,

- the bottom 50% hold only ~5–6% of total wealth and remain highly consumption-sensitive.

Healthy economies require middle-layer confidence — not just elite spending.

3. MSMEs Must Become Shock Absorbers Again

MSMEs contribute:

- nearly 30% of GDP,

- ~45% of exports,

- and support over 110 million jobs.

Yet many continue facing:

- high borrowing costs,

- delayed payments,

- weak domestic demand,

- and compliance burdens.

If India wants resilience against forex and employment shocks, MSME growth may need to outpace mere survival.

4. Export Intensity Must Deepen

India’s merchandise exports remain near the $450–500 billion range, but import dependence — especially oil, electronics, gold, and defense — continues exerting pressure on the current account.

A structurally stronger export engine would likely require:

- higher manufacturing depth,

- stronger electronics ecosystems,

- logistics efficiency,

- and greater MSME global integration.

Because sustainable rupee stability ultimately comes from stronger dollar earning capacity.

5. Energy Dependence Must Decline

India still imports roughly 85% of crude oil requirements. That means every major geopolitical disruption quickly becomes:

- an inflation event,

- a fiscal event,

- and a currency event.

Reducing energy vulnerability through:

- renewables,

- domestic manufacturing,

- EV ecosystems,

- nuclear,

- strategic reserves,

- and stronger domestic exploration capacity

is increasingly becoming macroeconomic stabilization policy — not merely climate policy.

At the same time, the system faces a deeper capital-allocation dilemma: The state-owned energy companies such as ONGC often remain important sources of government dividend income and fiscal support, even as long-term energy resilience may require significantly larger reinvestment into exploration, production, and future-proofing domestic capacity.

- ONGC’s dividend payouts to shareholders, including the government as majority owner, have risen substantially over recent years, with annual dividends in some recent periods reaching roughly 2–3x levels seen a decade ago, even as India continues depending on imported crude for nearly 85% of its oil needs

6. Fiscal Flexibility Must Be Preserved

The government is simultaneously attempting to:

- sustain infrastructure expansion,

- maintain welfare commitments,

- modernize defense,

- and reduce fiscal deficits toward ~4.4% of GDP.

That balancing act leaves limited room if:

- oil spikes,

- global growth slows,

- or capital outflows intensify.

The key risk may therefore not be immediate crisis —

but shrinking maneuverability.

7. Institutional Trust Must Rise Faster Than Narrative Intensity

Currencies ultimately reflect confidence. Not just reserves.

Confidence of high order needed in:

- governance quality,

- institutional stability,

- policy continuity,

- and economic credibility.

For there is critical need to:

- strengthen employment generation

- stimulate broad-based consumption

- Strengthen small and medium industries

- improve fiscal transparency

- reduce dependence on imported energy shocks

- protect middle-class purchasing power

- communicate tradeoffs honestly

- distinguish temporary restraint from permanent slowdown

Because confidence is not maintained through speeches and slogans alone, it is maintained when citizens feel the future expanding — not contracting.

Signal-Talk Take / Behind the Signal: Editorial interpretation based on system behavior, not sentiment

The important question may not be:

“Why is the government speaking about restraint?”

The deeper question may be:

“What kind of economy requires repeated emotional preparation from its citizens?”

Because when confidence changes tone, systems are usually trying to buy time

— aided by television panels, political emissaries, and narrative machinery designed to stabilize perception faster than fundamentals.

The real test is whether that time is used to deepen resilience —

or merely extend the narrative

Axiom In stable systems, governments generate confidence naturally - to promise prosperity. In stressed systems, they increasingly need to narrate it - to prepare citizens for restraint.

Signal-Talk Analysis: ST 033/ Indian economy – When the tone changes.

NV Subba Rao is the author of Uncle Sam 2.0 — a social media and systems-level exploration of power, media, and democracy in the algorithmic age.

Available on Amazon

Website: UncleSam2.com